Chapter 9: International Trade

International Trade:

With all of the markets we have studied so far we have assumed that the relevant prices are created within that specific market. In order to use the ordinary supply & demand model we have considered a single product or service and a single price created within that market through the mutual interdependence of buyer and seller behavior. A near exception is the case of price controls where we introduce an externally imposed price on that specific market. If a price floor is set above the original equilibrium we get a surplus (Qs > Qd) and if a price ceiling is set below the original equilibrium we get a shortage (Qd > Qs). We can borrow similar logic to analyze markets with international trade.

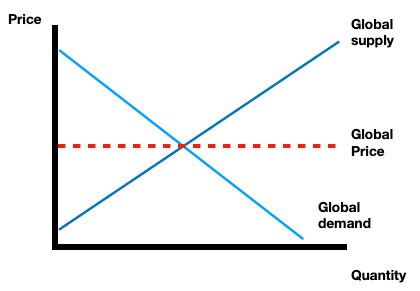

Our starting point is the global market or the world market for that particular product or service. Here’s the graph:

In the world market the demand curve is the global demand and the supply curve is the global supply. The equilibrium price that results is called the world price. This is the key price that will prevail in any market with free trade. For this reason in the graphs below I will draw the global market in the left panel and the domestic market in the right panel with the global price running straight across to enter the domestic market.

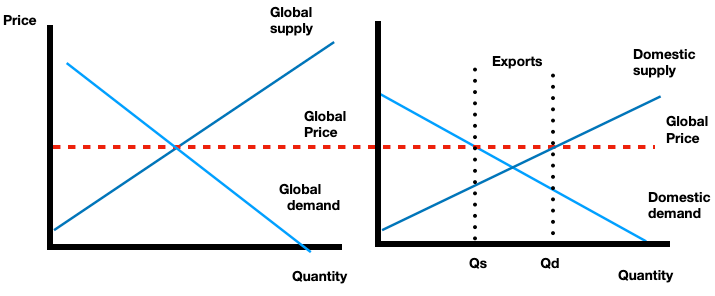

First we will consider the case of exports and then we will consider the case of imports. In doing so we will want to compare the quantity demanded and quantity supplied the results at the world price versus at the intersection of the domestic demand and domestic supply to crease the domestic equilibrium.

Because we are assuming that relative to the domestic market there’s unlimited goods available at the specific global price we are thinking of the global price and global supply as a horizontal line.

In the case of exports:

If the domestic price is below the world price, local producers hold a comparative advantage in producing that product. However, when the global price is higher than the domestic equilibrium price, domestic producers have an incentive to bypass their local market and sell their products abroad. At the higher price, overall domestic production increases and we represent this with an increase in (domestic) quantity supplied. But at the higher price domestic consumers are less interested in purchasing the product so we get a decrease in (domestic) quantity demanded. Basically local consumers are forced to compete with foreign consumers and the firm will sell its output to the highest bidder.

We can borrow some intuition from a binding price floor that does not allow prices to fall below that amount. Due to the presence of foreign buyers, the domestic market price does not fall below the price foreign buyers are willing to pay, the global price. Rather than getting a surplus as we would if this horizontal line were a true price floor, instead the excess units get sent abroad.

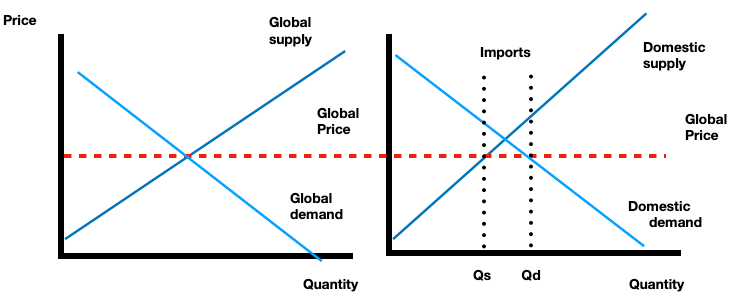

In the case of Imports:

If the local price is higher than the global price, the domestic producers lack a comparative advantage. Domestic buyers have an incentive to purchase the goods from foreign producers. This forces domestic producers to compete with foreign producers. As a result the domestic quantity demanded increases because buyers are willing to purchase more units at the lower price. At the same time the domestic quantity supplied decreases as fewer domestic producers are able to be profitable at the lower price.

We can borrow some intuition from a binding price ceiling that would not allow the price to rise higher than the ceiling. Similarly the availability of products available at the low world price provides no reason for domestic buyers to pay anything higher. Rather than getting a shortage, those units are imported to make up the mismatch between the domestic quantity demanded and domestic quantity supplied.

Generally speaking with any price change (or policy change) there are winners and losers. In the case of free trade we have the outcome that ‘winners win more than losers lose’. This is another way of saying that free trade is efficient, that overall economic value created has increased when we move to free trade.

In the case of exports, domestic consumers lose out because local firms bypass them to sell to foreign consumers instead. So domestic consumer surplus falls. But because those foreign consumers are willing to pay more and because the quantity supplied increases, domestic producer surplus increases to more than compensate for the loss of consumer surplus. The winners (domestic producers) win more than the losers (domestic consumers) lose.

In the case of imports, domestic producers lose out because local consumers opt to purchase from foreign firms instead. Domestic producer surplus falls because they’re unable to compete with foreign firms. They have to cut prices and reduce their quantity supplied. For this reason domestic producer surplus decreases. But domestic consumers get such a great deal on those units and they’re able to purchase so much more that domestic consumer surplus increases more than domestic producer surplus has fallen. The winners (domestic consumers) win more than the losers (domestic producers) lose.

Importantly these ‘gains and losses’ are not spread evenly throughout the market. In the case of imports:

Gains to domestic consumers are widely dispersed across all buyers of the product now able to obtain more of the good at a lower price

Losses to domestic producers are highly concentrated among the domestic producers that lose business to lower-priced goods from more efficient foreign rivals.

In the case of exports:

Gains to domestic firms are highly concentrated amongst a few domestic producers that are able to ramp up production to export abroad finding new foreign buyers

Losses to domestic consumers are widely dispersed across all prospective buyers who are now bypassed when goods are diverted out of the domestic market into the foreign market.

Basically in both cases each consumer is affected a little, though the total effect may be large when aggregated across all consumers; each producer is affected a greal deal, though these effects are concentrated in then hands of a few firms. This is relevant for the large amount of bargaining power (and lobbying power) that firms enjoy and the relatively weak bargaining (and lobbying) power of consumers.